Victoria Hernandez, Board Member (NED) CaixaBank Payments and Consumer

The banking industry is undergoing a major transformation. The industry faces challenges and opportunities on many fronts – from the pandemic recovery, the growing competition from technology companies, the call to respond to the threats of climate change, to the increasing request of regulation.

This presents the sector with both challenges and opportunities. It also makes the role of risk managers extremely complex. But there are ways that banks can ensure they make the most of this upheaval and come out of this transformation as leaders in sustainable financial services. I believe the way forward is for banks to build on their existing customer relationships and knowledge, to join with policymakers and businesses in setting the agenda to solve the biggest issues facing Europe’s, and the global economy. By getting out on the front foot, taking on their new competitors in a responsible way, banks will renew their sense of purpose, ensure their ongoing relevance, grow the bottom line, and reap the benefits of demonstrating a real commitment to ESGs. I would like to highlight some of the many issues that banks are now facing and offer some thoughts on how a new banking culture based on diversity, transparency and ethics, can provide the solutions and the way forward.

Digital transformation of financial services

The banking sector is facing the most competitive and challenging business environment it has ever seen, due to the rapid digital transformation of financial services and the entry of non-traditional financial services providers into the market. At the same time, the highly regulated sector is facing the new demands of strict privacy and data regulation, coupled with the increasing expectations of consumers.

The barriers to entry into financial services have been considerably lowered because of digital technology, which has enabled the list of new financial services providers to grow exponentially in recent times. Neobanks, Fintechs, BigTechs, cryptocurrency exchanges – each one of them is disrupting the concept of banking and traditional financial institutions are either competing with them or in some cases investing and/or cooperating with them to improve their customer experience.

While many of Europe’s banks have lagged behind their international counterparts in adopting digital technologies, being driven by prudence and attention to detail and therefore culturally resistant to change. Nevertheless, banks are aware that they must respond to their changing business environment by keeping pace with technological change and deploying it in their own organisations, while also adapting their skillsets and mindsets through a conscious program to be more diverse and inclusive.

Balancing the banking needs of the generations

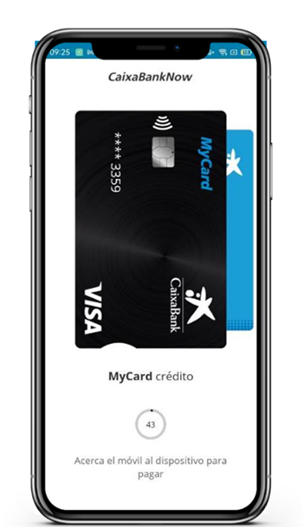

The major advance which has been changing the customer’s banking experience in recent times has been the switch to online and mobile banking. This started well before the pandemic but has accelerated over the last two years. In today’s era of unprecedented convenience and speed, and the need to be kept socially distanced where possible, many consumers don’t want to go to a physical bank branch to handle their transactions. This is especially true of Millennials and the older members of Gen Z, who have started to become the dominant players in the workforce (and the biggest earners).

Critically for banks, many studies show that at least 60% of mobile banking users research a bank’s mobile capabilities before opening an account, and a similar number say they would change banks if their bank offered a poor mobile banking experience. On the other hand, the Baby Boomer generation disproportionately prefers a traditional banking experience. To satisfy all of these customer requirements, banks face a delicate balancing act – offering fulfilling and responsive online experiences while also maintaining sufficiently well-staffed physical bank branches too.

But more than just a change from real to virtual banking, we’ve now reached the point where simply having a mobile app isn’t enough for banks to attract and keep customers. Additional tools and features – such as two-factor or one-time authentication processes, the ability to put temporary holds on cards, view recurring charges, or scanning a fingerprint to log into an account – are becoming increasingly necessary and expected.

From my many years of experience in both the finance and telecommunications industries, I know that digital transformation of the banking sector is inevitable, but I also recognise that its success will rely largely on the degree of cultural change and renewal that the banks are able to achieve. The leading banks are learning how to embrace a new way of thinking and are adopting a range of approaches which seek to manage all of these risks, while at the same time, refocussing their efforts on their customers.

Providing customer-first services

The pandemic has accelerated banks’ digital agendas and has prompted them to rethink their transformation journeys with

the goal of capturing new growth opportunities and creating more intelligent customer experiences. But regardless of their level of digital transformation, banks should be making better use of data to build out their ecosystem and create superior offerings for customers.

Banks will have to compete in new ways as finance becomes embedded in customer-first services. The pandemic has accelerated changes in the way banking products are delivered, moving them closer than ever to customers’ point of need. Payments, lending and other banking products are increasingly being delivered in ecosystems that serve a wider set of customer requirements. If banks can’t create new ecosystems themselves, they can serve as providers of finance to existing networks. If they do not respond, banks will see more market share shifting to fintechs and big tech companies.

Banks have a key advantage over new fintechs and purely online financial services. They already have deep relationships with their customers and can apply automated systems which maximise profit. They are well placed to assist their customers in managing their funds and their expenditure, as a trusted, reliable partner in the financial world. For example, if unexpected expenditure occurs, outside the normal pattern of the customer’s daily life and routine, the bank can recognise this automatically and alert the customer of a potential fraud, or partner with the customer to ensure that spending limits on certain items or activities are not exceeded.

In contrast, some newer fintech companies lack these insights into customer behaviour and expectations and may not be seen as putting the needs of the customer first. Buy Now, Pay Later (BNPL) services provide a type of credit in the guise of a payment mechanism, which could potentially trap an unwary consumer into high interest rate payments that can become difficult to pay off. Banks need to ensure that they differentiate themselves and behave in a way that is transparent in terms of their fees and payment options, and that they remain ready to assist customers who may have difficulty paying bills during unexpected life changes, such as recent pandemic lockdowns.

Driving innovation

Banks are increasingly supporting the innovation economy through special products and programs aimed at encouraging tech start-ups and SMEs, especially those who are working in sustainable industries. For example, CaixaBank has partnered with the European Innovation Council in a new pilot, the first of its kind in Europe, that calls for the most innovative European startups to respond to the main challenges of the agricultural sector and bring solutions to final consumers with the specific support, expertise and selling channels of the largest bank in Spain and one of the largest in Europe.

Banks are also responding to the needs of their eco-conscious clients by becoming more aware of their environmental footprint and the importance of sustainable practices. Banks are estimated to issue over 6 billion plastic cards annually, so switching customers to mobile payment methods will reduce the environmental impact of financial services. I am pleased to say that CaixaBank was the first financial institution in Spain and one of the first banks in the world to issue its cards in alternative materials, with less impact on the environment. It is also a market leader in digital payments.

Banks are also recognising the importance of small-to- medium enterprises (SMEs) to the global economy and are developing new products and services tailored at the needs of this underserved market. SMEs are often hit with late payment for services and long invoice maturity, which can hamper both short-term agility and long-term growth and investment. Agile banks are developing solutions that would help raise finance against already-issued – but as yet unpaid – invoices, better management of SMEs’ cashflow capabilities.

Banks should evolve their existing technology and platforms to ones that use advanced machine learning models, to generate tailored insights in real-time, within context. Banks can harness the power of advanced analytics and robotic process automation to transform the way trade finance teams identify and control risk, including by detecting patterns of illicit trade finance activity. Many are now partnering with telecom operators to share data and to deploy the latest risk analytics tools, leveraging natural language processing, text analytics and third-party data to underpin a risk analytics scoring engine which can support the analysis of large volumes of trade transactions. In adopting these new technologies, banks should also ensure that their use of data and AI is transparent and explainable to the customer, who can weigh up the benefits against any concerns they may have. Banks must also, of course, in all handling of customer data, adhere strictly to the GDPR in Europe, and any other regulatory or legal obligations on privacy and data security where they operate.

A new culture of banking – ethical fintech

Digital technology has transformed the banking sector, and for many more traditional banks, they are facing a need to reinvent themselves and their culture – to embrace diversity and inclusion, to foster innovation and new ways of thinking, and to encourage transparency and new levels of trust with their customers. As regulated entities, banks must also strictly adhere to ‘responsible lending’ practices, in accordance with the current legal framework, to guarantee an adequate level of protection for their customers. This combination of innovation and risk management is ultimately their main competitive advantage, and one which sets many banks apart from new fintech entrants.

Bank executives also have a clear opportunity to lead the creation of an authentic, differentiated identity that embeds an ethical purpose. This is important, as many banks have yet to turn their commitments to environmental, social, and governance (ESG) concerns into concrete action. The UN Principles of Responsible Banking1, to which CaixaBank is a founding signatory, are a unique framework for ensuring that banks’ strategy and practice align with the vision that society has set out for its future in the Sustainable Development Goals and the Paris Climate Agreement. Every customer should check if their own bank adheres to this UN Charter. In the same way that we avoid buying goods manufactured by children, consumers should become part of this ethical movement to ensure that banks are working for the common good.

In summary, banks must move quickly toward developing digitally advanced products and customer engagement practices. Banks must view disruption as an opportunity to phase out legacy systems in favour of new operating models. Now, more than ever, banks need to play to their strengths and embrace change at the pace and scale that will drive the best results for both their shareholders and their customers. I am convinced they can do this best through a clear focus on ethics, sustainability, trust and personalised customer service.

Victoria Hernandez is non-executive Director (NED) at CaixaBank Payments & Consumer, the top bank in Spain and one of the largest banks in Europe. Judge at the European Commission, in charge of approving EU proposals for the European Innovation Council (EIC) Horizon Europe funding applications. Likewise, she represents the interests of the EIC €10,5bn fund as NED in the Belgian telecommunications company, Tessares. She is also NED of TeamEQ, an AI & ML powered service that offers solutions in the field of human resources, and a member of the advisory board of Cashway, a financial technology company. Previously, she was Alliance’s Director British Telecom Europe, Executive Chairman Orange Spain and Senior Vice-President international Proximus. Victoria holds a Bachelor of Engineering in Computing Sciences from UPC, EMBA at INSEAD, a Masters Degree in Digital Marketing from Columbia Business School, and of Financial Technology from Harvard University. Victoria lives in Paris and speaks 5 languages fluently. She has one lovely daughter (Rita).