VICTORIA HERNANDEZ

Rising Tide Europe 3, Head of the Investment Committee

There is a growing trend to believe that the future of cash is limited, with a number of developed countries stating their intention to become fully cashless within a few years. This seems like an inevitable consequence of digitalisation of the financial services sector, but is this the whole picture of our digital future, and if so, what implications will that have for society as a whole?

According to the European Banking Federation, almost 50,000 bank branches have been closed across the EU over the past decade (21%). Banks are under pressure to transform their business model in line with the new financial services market and have been investing heavily in digital transformation of payment infrastructure and services. These figures reflect a broad trend in Europe towards restructuring and consolidation across the branch networks of banks, as digital and mobile delivery channels prove increasingly popular with customers.1 The large scale of bank branch closures in recent decades has left millions of people struggling to access the vital financial services and cash that they need. Bank branches are essential business supports for small business owners whose customers prefer to pay cash or in areas where internet services are insufficient, or indeed where the elderly or those with disabilities may not have either the skills or the confidence to use internet banking.

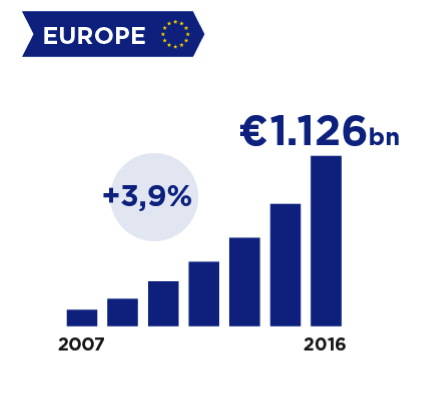

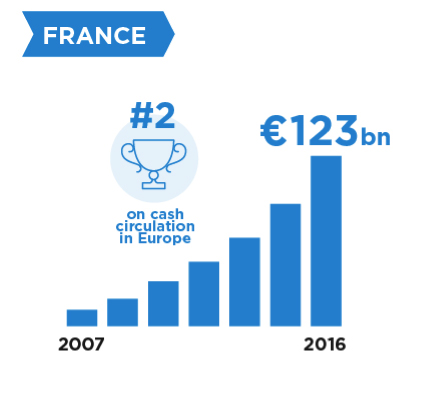

Table 1. Cash circulation in Europe (Source : Banque de France)

Despite a general perception to the contrary, the use of cash is widespread in most European countries. According to the European Central Bank, in 2016 cash was the dominant payment instrument in the 19 countries of the Euro area. In that year, Euro area consumers made more than €1,870 billion worth of transactions by means of cash, which represents 79% of all transactions or 54% of the total value of all payments. Most of these payments were made in shops for day-to-day items, restaurants and petrol stations, as well as at street merchants and shops for durable goods.2 The chart on above shows how paper money (cash) in circulation has been consistently growing year over year in Europe. (The same bank note can be used again in multiple payments, which explains the difference between €1,870 billion cash payments and €1,126 billion cash in circulation.)

While larger retailers have embraced digital transactions, small family-based retailers and SMEs who rely on cash payments from their customers, are increasingly being left with difficulties in handling and managing their cash. In addition, these trends are acting together to increase the financial and social marginalisation of large sectors of the European community. In 2016, there were 118 million people in the EU-28 who lived in households at risk of poverty or social exclusion,3 equivalent to 23.5 % of the entire population4. In times of economic hardship, many consumers rely on cash to manage their budgets more carefully and bank services are too costly for them.

It is important to keep in mind that a cashless society relies on three things to work: networks, electricity and security. In times of natural or man- made disasters, where digital currency is not available, cash is often the only fall-back solution. The US Government’s disaster management agency, FEMA , for example, advises those preparing for hurricanes to make sure they have plenty of cash in large and small bills for when there is a power blackout and online payment systems or automatic cash dispensers are of offline.4

MARKET TRENDS

Historically, banks with the best branch footprint have dominated their markets, gaining outsized share. In few years, all banks will be direct banks, and branch banking will be changing fast. Leaders will offer an anytime, anywhere service, fully utilising all banking channels in an integrated fashion. They will be re- imagining their physical footprints, introducing new branch formats, expanding physical points of presence through third-party partnerships, driving sales and cutting costs. Where branch networks are thinner, physical distribution will continue to evolve, and banks are more likely to partner with new-entrants to create alternative distribution channels. 5

Banking the unbanked (urban and rural) will become a primary policy objective in both developed and emerging markets, as governments seek to reap the economic benefits of broader access to financial services for their populace. This push will drive new products and business models and will become the primary focus of governmental or state-sponsored institutions, particularly where the private sector is unable to fulfill the need.

Paper money or cash is issued and backed by Central Banks. It is an instant mode of payment with no transactional cost for the end-user. The disappearance of cash will represent to leave the whole payment system in private hands: the banks. With time, Central Banks might issue digital cash of legal tender (i. e. digital euros) but this represents a major change in the Banking regulatory system and to implement a radically different technology, new processes and skills in place which might take many years.

In summary, the closure of Bank branches is a European-wide trend, which is having many negative consequences for SMEs, the rural and isolated as well as the poorer in our communities. The digital transformation of the Banking industry, while having many positive effects in terms of efficiency and business stimulation, is also creating a digital divide and excluding some of the most vulnerable.

THE FUTURE OF CASH

So what is the future of the digital transformation of cash, and the seemingly inexorable rise of cashless digital banking? Countries which are far advanced in the transition towards a cashless society are experiencing a backlash from the very communities which rely on cash on a day to day basis.

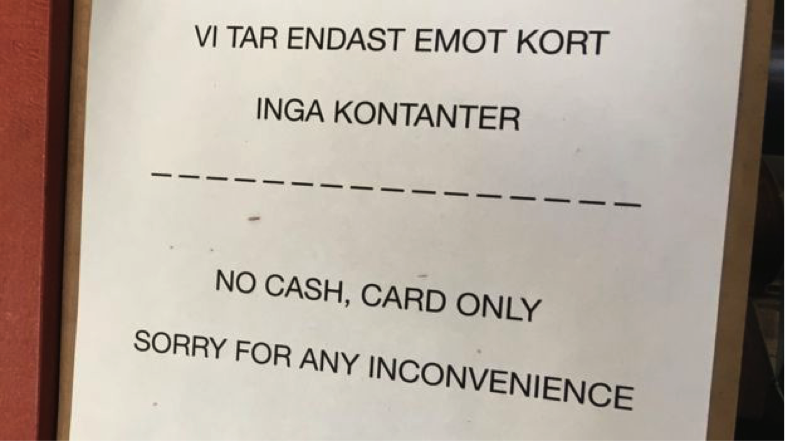

Many Swedish shops and restaurants now only accept card or mobile payment systems. Source; BBC online news (https://www.bbc. com/news/business-43645676)

Sweden is often touted as the example of the world’s first completely cashless society. However, there is growing concern amongst those representing vulnerable groups, who believe that the move to getting rid of physical cash is going too fast for many to keep up.

Most high street stores, cafes and public transport in Stockholm no longer accept cash, while most Swedish banks have stopped dealing in cash over the counter, having phased out cheques long ago. At the same time, fees for in-bank transactions have steadily increased.

Similarly, in Australia it has now become unusual, especially for younger people, to use cash, many now using ‘tap and pay’ for most day to day purchases. Australia’s central bank also recently declared6 that currency was likely to become a “niche payment” used only in emergencies, while cheques would be phased out altogether.

THE CASE FOR REAL DIGITAL CASH

So if the banks and governments in many countries are heading towards a cashless future, what can be done to help small business and vulnerable groups to cope with the transition? Will they be left without the means to undertake many of their daily tasks? The key to the transition from a fully cash to a digital society lies in implementing a solution which combines the best of both worlds – the efficiency and immediacy of digital payments systems with the convenience and perceived security of physical cash. This type of solution is being offered by start- ups like CashWay7 which offers an SaaS- based solution for financial institutions and consumers. CashWay enables virtual retail banking, thus solving the problems mentioned above: banks can deploy a virtual network of branches quickly and at marginal cost where SMEs can make cash deposits, while consumers can make online purchases and pay for them with cash.

By ensuring that the benefits of physical cash are preserved, we can support the vulnerable and less digitally literate in our digital society, without leaving them behind. This should be the goal for all of us involved in digital transformation.

Victoria Hernandez is a highly recognized senior executive with more than 25 years’ experience in building, launching and managing multinational enterprises in the EU and globally, primarily in the TMT and the Fintech services sector. She is Former Alliance’s Director BT Europe, Executive Chairman Orange Spain and SVP international Proximus.

Victoria is an entrepreneur, speaker at international conferences and Business Angel. She is currently Head of the investment committee of Rising Tide Europe, an investment program run in cooperation between EBAN, GO-Beyond Investing and the Next Wave Foundation, part of a global movement to increase women’s participation in angel investing as an asset class. She is a Horizon2020 EIC Instrument Judge Expert at the European Commission, evaluating EU proposals for H2020 funding, a Judge member of MIT review under 35 and Non-Executive Director of several organizations and companies.

She is also a member of the Board of the Global Telecommunications Women’s Network (gtwn.org) the international forum for executive women in technology to contribute to the evolving global information society in a positive manner. A Computer Engineer, with an EMBA from INSEAD and a Masters in Digital Marketing from Columbia Business School. Victoria lives in Paris and speaks 6 languages fluently.

- Source: European Banking Federation – Sept. 2017 Facts and figures

- Source: ECB – The use of cash by house- holds in the euro area. Nov. 2017

- Source: AROPE

- https://www.fema.gov/disaster/4339/hurri- cane-preparedness

- PWC – Retail Banking 2020 Evolution or Revolution

- https://www.smh.com.au/politics/federal/ cashless-future-australia-swish-notes-swe- den-20181129-p50j21.html

- https://www.cashway.fr/home/